Published May 17, 2024

What's Up With Real Estate for the Week of May 19th

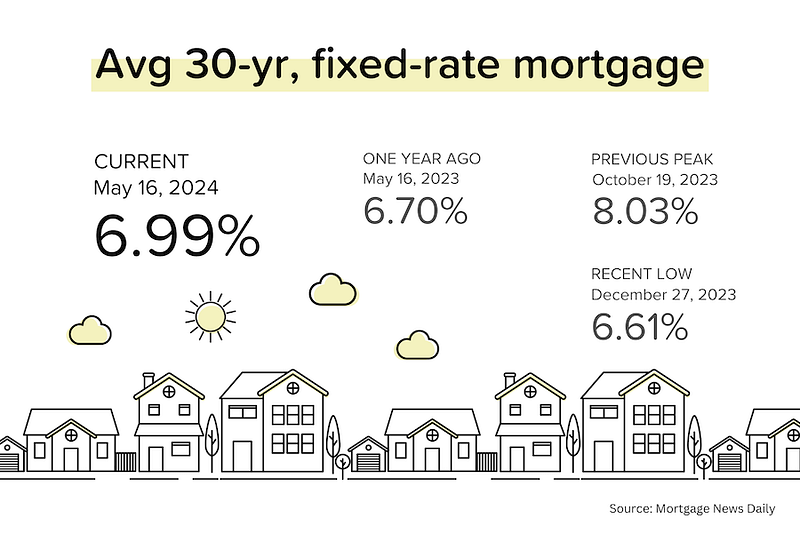

Lower mortgage rates were as easy as 1–2–3 this week! A string of bond-friendly data releases (BLS jobs, retail sales, CPI inflation) propelled average 30-yr mortgage rates back below 7%. If this can hold, it should boost transaction volumes (existing & new homes) in the coming months.

#1: Slower job growth. This happened last week, but just to remind you: April employment grew by 174K, much lower than the 240K expected. The unemployment rate also rose from 3.8% ? 3.9%. [BLS]

#2: Flat means down. April retail sales were flat month-over-month and the growth in March was revised down from +0.9% to +0.6%. Keep in mind that the retail sales figure is not adjusted for prices. Why is retail sales so important? Because consumer spending drives the US economy. Slower GDP growth ahead? [Census Bureau]

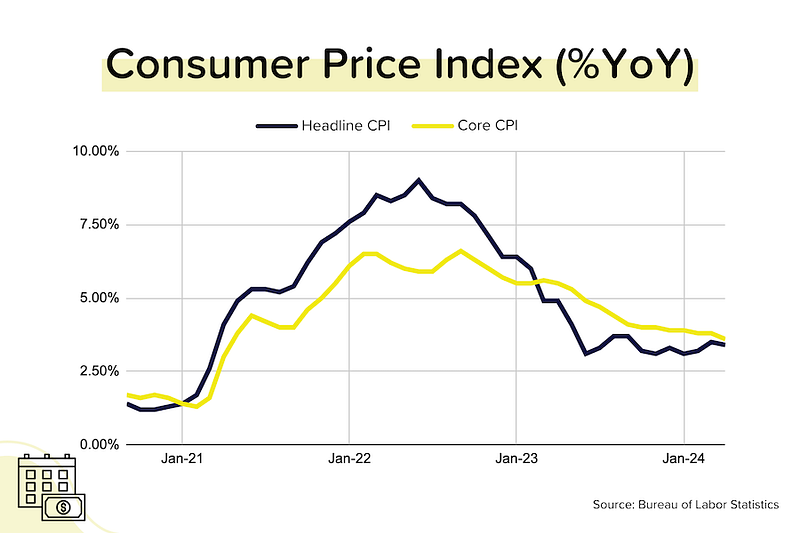

#3: Cooler inflation. The “core” (ex-food & fuel) Consumer Price Index for April rose 0.3% MoM and +3.6% YoY (down from +3.8% YoY in March). Nearly ALL of the increase in the index came from two items: Shelter costs and car insurance. [BLS]

Note: NONE of these individual figures screamed ‘recession ahead!’ 3.9% is still a low unemployment rate, 3.6% YoY inflation is still too high for the Fed, and one month of flat retail sales isn’t a disaster. It’s just that the bond market had become so pessimistic—one or maybe zero rate hikes priced in for 2024—that all it took was a bit of good news to drive a reversal in sentiment.

Speaking of sentiment. The University of Michigan’s consumer sentiment index plunged to 67.4 in May (from 77.2 in April). This was well below expectations and is the lowest figure since November 2022. Consumers were more worried about inflation, and nearly 40% of respondents see the unemployment rate rising further from here.

Higher rates put a nail in builder confidence. With average 30-yr mortgage rates up more than 50 basis points (0.50%) in April, is it really any surprise that builders were less bullish? The National Association of Homebuilders confidence index dropped from 51 in April to 46 in May. Anything less than 50 is bearish/contractionary.

Note: This index will almost certainly recover next month if mortgage rates can hold below 7%.

That’s constructive. April housing starts rebounded 6% MoM to 1.36 million units (SAAR), but that was below expectations. Completions, however, jumped 9% MoM to 1.62 million units (SAAR). Permits were down 3% MoM to 1.440 million units (SAAR).

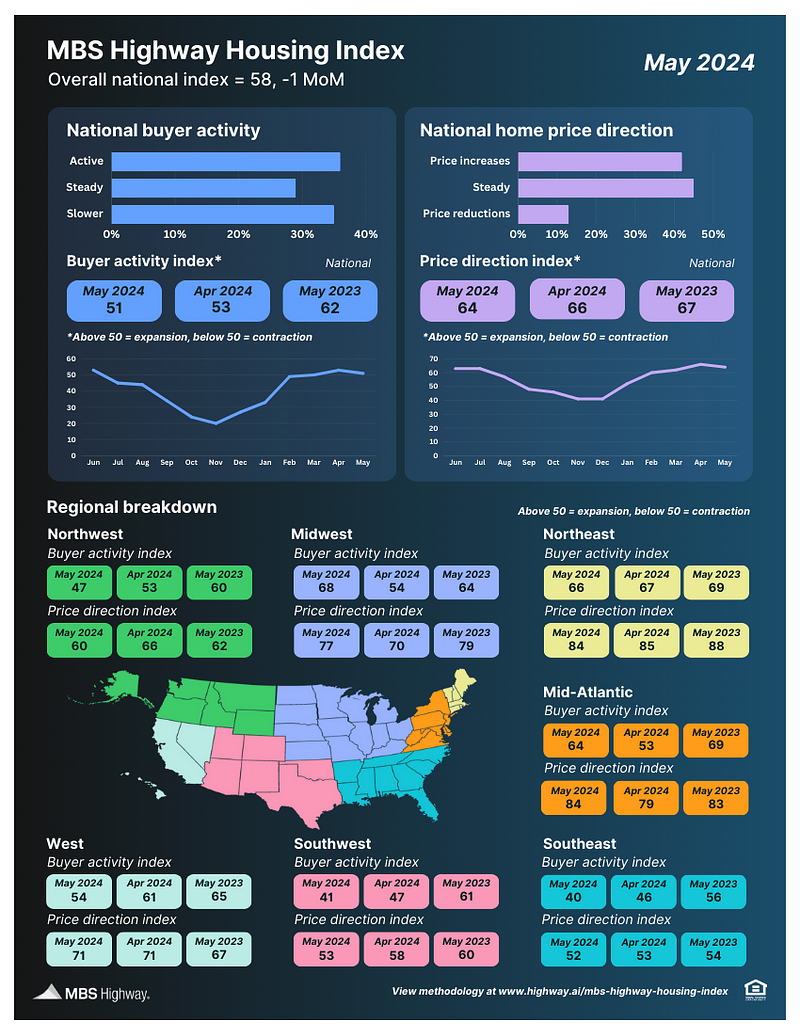

MBS Highway Housing Survey Results for May

Every month our parent company, MBS Highway, surveys LOs and real estate agents to get their 60-second takes on their local housing markets. Here are the results for May:

National Index

- The National Housing Index dropped 1 point to 58 in May 2024, from 59 in April 2024. This was the first month-over-month decline experienced since November 2023. In comparison, the index rose 13 points to 64 in May 2023, from 53 in April 2023.

- This unseasonal decline was driven by a more than 50 basis point (half a percentage point) rise in average 30-year mortgage rates over the course of April. Our survey was conducted at the start of May, when mortgage rates were near 7.5%.

- Both the Buyer Activity (53 - 51) and Price Direction (66 - 64) sub-indexes eased by 2 points in May 2024. This is in contrast to the +5 MoM gain in the Buyer Activity index and the +17 MoM jump in the Price Direction index seen in May 2023.

Regional Indexes

- While most regions (5 out of 7) saw declining Buyer Activity levels in May 2024, the Midwest surged ahead (54 - 68) to become the country’s most active region for the first time. Not far behind, the Northeast (67 - 66) remained strong, while the Mid-Atlantic (53 - 64) closed the gap with the frontrunners.

- The Northwest (53 - 47) saw its Buyer Activity sub-index slip below 50 in May 2024, joining the Southeast (46 - 40) and Southwest (47 - 41) as the least active regions. Even the recently resurgent West region fell month-over-month (61 - 54).

- Although the Home Price Direction sub-indexes dropped in 4 out of 7 regions, prices were still generally trending higher (index levels >50). The biggest jumps were seen in the Midwest (70 - 77) and Mid-Atlantic (79 - 84) regions. The biggest falls were in the Northwest (66 - 60) and Southwest (58 - 53) regions.

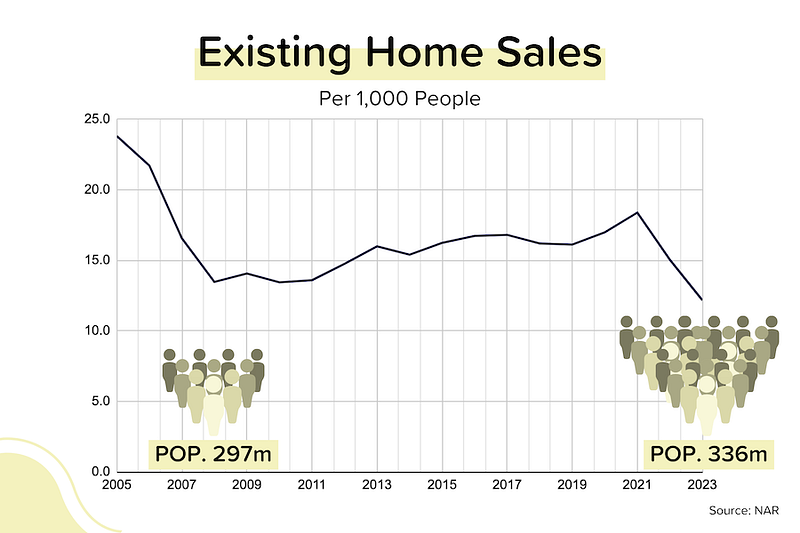

The Inevitable Snapback

A few weeks ago, I looked at existing home sales on a per person basis. It’s a simple idea: if your population is growing, you should have more homes changing hands, all else being equal. Well, we sold 4.1 million existing homes in 2023, about the same as we did in 2008. That’s already a crazy low figure (the pre-COVID average was 5.2 million). But when you add in the fact that the US population has grown by 40 million over the same time, it gets ridiculous!

Mortgage Market

Average 30-year mortgage rates have dropped from over 7.5% to below 7% in just over two weeks. The magnitude and speed of the decline almost perfectly matches the increase seen in early April. We’re basically back to where we were before the (bad) March CPI data came out (on April 10) and sent bonds into a tailspin.

Current odds on Fed rate cuts at upcoming FOMC meetings below. Keep in mind that the US Presidential election is on November 5. The Federal Reserve is meant to be independent and apolitical, but a rate cut on Sept 18 would certainly look political, even if it was warranted. Hmmm.

- Jun 12: 6% (fairly steady from last week)

- July 31: 28% (fairly steady from last week)

- Sept 18: 66% (fairly steady from last week)

- Nov 7: 79% (up from 77% last week)

They Said It

“April was a tough month for buyers, with mortgage rates up a half-percent on stubborn inflation data. Despite this, our MBS Highway National Index only dropped by a single point in May, reflecting resilient demand and limited inventory in most markets,”—Barry Habib, MBS Highway’s Founder and CEO

“Moving forward, the multifamily market will see additional declines for construction volume, while the pace of completions remains elevated. April marked the fifth consecutive month for which the seasonally adjusted rate of multifamily completions was above 500,000. This additional rental supply will help lower shelter inflation, which is the last leg of the inflation policy challenge.”—Robert Dietz, NAHB’s Chief Economist